Fixed vs. variable interest rates takes center stage in the financial world, offering unique opportunities and challenges for borrowers and investors alike. In this article, we delve into the intricacies of these interest rate options to help you make informed decisions.

Exploring the key differences between fixed and variable interest rates, understanding how economic factors influence them, and uncovering the risks and benefits associated with each type will provide you with valuable insights into navigating the complex landscape of interest rate choices.

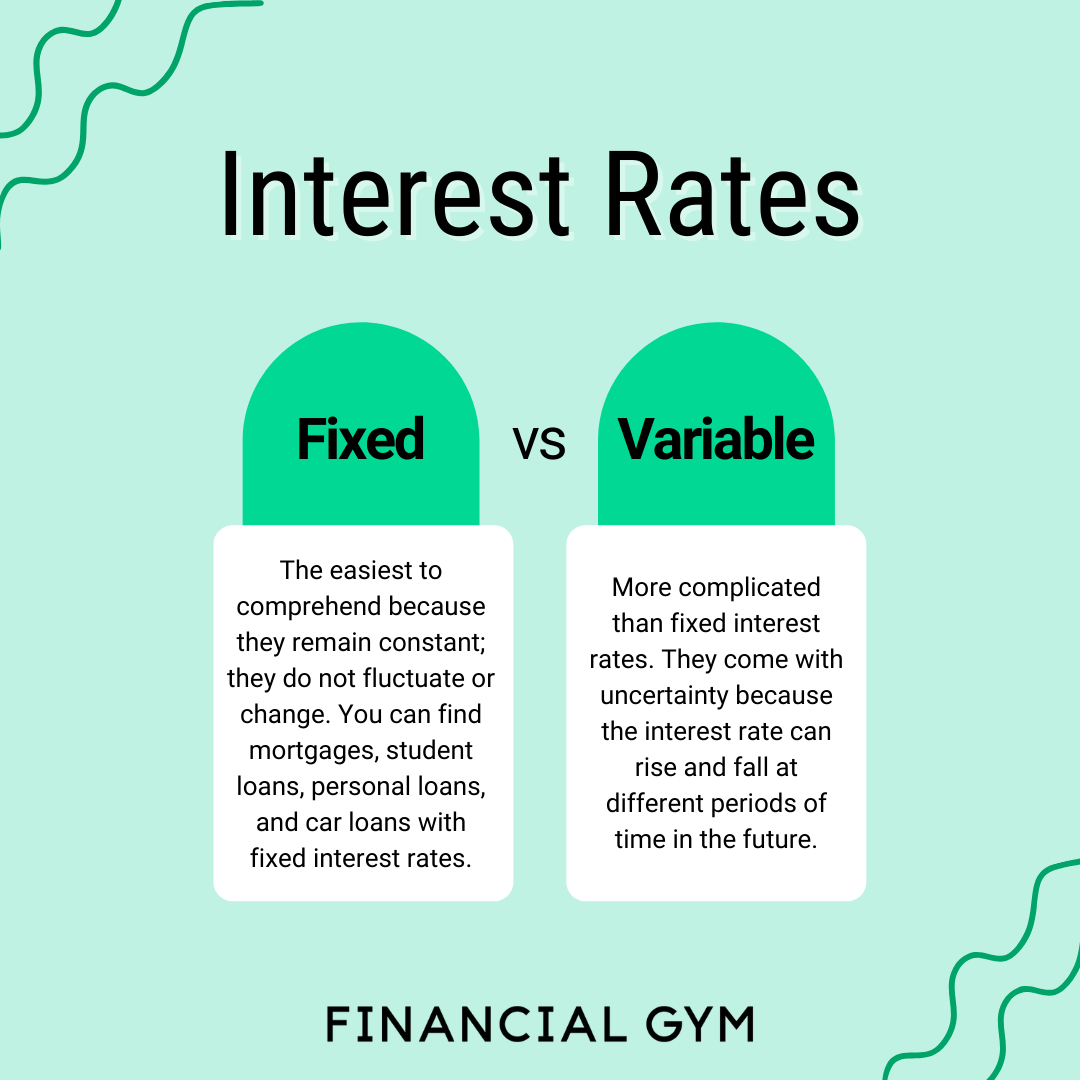

Fixed vs. Variable Interest Rates

When it comes to loans or mortgages, borrowers often have to choose between fixed and variable interest rates. Let’s explore the differences between the two options.

Fixed Interest Rates

Fixed interest rates remain the same throughout the entire term of the loan. This means that your monthly payments will also remain constant, providing predictability and stability in your budget.

- Advantages of Fixed Interest Rates:

- Protection against interest rate hikes: With a fixed rate, you are shielded from sudden increases in interest rates, which can help you plan your finances better.

- Predictable monthly payments: Knowing exactly how much you need to pay each month can make budgeting easier and more manageable.

- Disadvantages of Fixed Interest Rates:

- No benefit from rate decreases: If market interest rates drop, you will not be able to take advantage of lower rates without refinancing your loan.

- Potentially higher initial rates: Fixed rates may be higher than initial variable rates, which could result in higher initial payments.

Variable Interest Rates

Variable interest rates, also known as adjustable rates, can fluctuate over time based on changes in market interest rates. This means your monthly payments can vary, making it harder to predict your future payments.

- Advantages of Variable Interest Rates:

- Potential for lower initial rates: Variable rates may start lower than fixed rates, resulting in lower initial payments.

- Opportunity for rate decreases: If market interest rates go down, your interest rate and monthly payments may decrease without refinancing.

- Disadvantages of Variable Interest Rates:

- Risk of rate hikes: If market rates increase, your interest rate and monthly payments can rise, leading to financial uncertainty.

- Difficulty in budgeting: The variability of monthly payments can make it challenging to plan your finances effectively.

Factors Affecting Interest Rates

Economic conditions, market forces, and central bank policies all play a crucial role in determining fixed and variable interest rates.

Economic Conditions Influence Fixed Interest Rates

Fixed interest rates are influenced by various economic conditions such as inflation, economic growth, and the overall stability of the market. When the economy is booming and inflation is high, fixed interest rates tend to rise to compensate for the increased cost of borrowing. Conversely, during economic downturns or periods of low inflation, fixed interest rates may decrease to stimulate borrowing and spending.

Market Forces Impact Variable Interest Rates

Variable interest rates, also known as adjustable rates, are directly impacted by market forces such as supply and demand for credit, investor sentiment, and the overall health of the financial markets. When there is high demand for credit or positive investor sentiment, variable interest rates are likely to increase. Conversely, if there is a surplus of credit available or market uncertainty, variable interest rates may decrease to attract borrowers.

Role of Central Banks in Determining Interest Rates

Central banks, such as the Federal Reserve in the United States or the European Central Bank in the Eurozone, play a significant role in setting short-term interest rates. By adjusting the federal funds rate or the discount rate, central banks can influence borrowing costs for financial institutions, which in turn affects the interest rates offered to consumers. Central banks use interest rate policies as a tool to control inflation, stimulate economic growth, or address financial stability concerns.

Risks and Benefits

When it comes to interest rates, borrowers and investors both face risks and benefits depending on whether they choose fixed or variable rates. Let’s explore the potential advantages and disadvantages of each option.

Risks Associated with Fixed Interest Rates for Borrowers

Fixed interest rates provide stability and predictability for borrowers, as the rate remains constant throughout the loan term. However, one major risk is that if market interest rates decrease, borrowers with fixed rates will miss out on potential savings. Additionally, borrowers locked into fixed rates may face penalties if they want to refinance or pay off their loan early.

Benefits of Variable Interest Rates for Investors

Variable interest rates are directly tied to market conditions, allowing investors to take advantage of lower rates when they decrease. This flexibility can lead to cost savings over time, especially if market rates remain low. Investors also have the opportunity to benefit from interest rate decreases without facing penalties for refinancing or paying off loans early.

Strategies to Mitigate Risks for Fixed and Variable Interest Rates, Fixed vs. variable interest rates

For borrowers with fixed interest rates, one strategy to mitigate the risk of missing out on savings is to consider a hybrid loan that combines fixed and variable rates. This option provides some stability while allowing borrowers to benefit from potential rate decreases. On the other hand, investors with variable rates can protect themselves by setting a cap on how high the interest rate can go, limiting potential increases in payment amounts.Overall, understanding the risks and benefits of fixed and variable interest rates can help borrowers and investors make informed decisions that align with their financial goals and risk tolerance levels.

Impact of Interest Rates on Investments

Interest rates play a crucial role in shaping the investment landscape across various asset classes. Let’s explore how changes in interest rates can impact investments in real estate, stock markets, and business decisions.

Real Estate Market

Changes in interest rates can significantly influence the real estate market. When interest rates are low, borrowing costs decrease, making mortgages more affordable. This often leads to an increase in demand for real estate, driving up property prices. On the other hand, rising interest rates can deter potential homebuyers due to higher borrowing costs, leading to a slowdown in the real estate market and potentially causing property prices to stagnate or decline.

Stock Market Performance

Fluctuations in interest rates can have a profound impact on stock market performance. In general, lower interest rates tend to be favorable for stocks as borrowing costs decrease, making it cheaper for companies to finance growth and expansion. This can boost corporate earnings and overall market sentiment, driving stock prices higher. Conversely, rising interest rates can increase borrowing costs for companies, potentially leading to lower profits and subdued stock market performance.

Business Financial Decisions

Businesses can leverage interest rate movements to make strategic financial decisions. For instance, when interest rates are low, companies may take advantage of cheaper borrowing costs to fund capital expenditures, acquisitions, or other growth initiatives. On the other hand, businesses may choose to hold off on borrowing or refinancing debt when interest rates are expected to rise, in order to avoid higher interest expenses in the future.

By closely monitoring interest rate trends and adjusting financial strategies accordingly, businesses can optimize their capital structure and improve overall financial performance.

In conclusion, the decision between fixed and variable interest rates ultimately depends on your financial goals, risk tolerance, and market expectations. By weighing the pros and cons carefully and considering your individual circumstances, you can choose the option that best aligns with your needs and preferences.

Answers to Common Questions

What are the main differences between fixed and variable interest rates?

Fixed interest rates remain constant throughout the loan term, providing predictable payments, while variable rates fluctuate based on market conditions.

How do economic conditions impact fixed interest rates?

Economic factors such as inflation, economic growth, and central bank policies can influence fixed interest rates.

What are some strategies to mitigate risks associated with fixed interest rates?

Diversifying investments, refinancing loans, and monitoring market trends are common strategies to manage risks with fixed interest rates.